The Rise and Fall of Billabong

We can trace Billabong back to 1973, when Gordon and Rena Merchant started sowing and selling board shorts in the Gold Coast of Australia. Billabong is an actual word that means some kind of oasis. They coupled the word with a wave design to form their iconic logo. The first few years in business, the duo carried out their operation from home, designing the shorts on their kitchen table and selling them in local surf shops. The demand for their products outgrew their home operation capacity and they switched to their first factory in 1975. The surf community adored Billabong’s products, and word of mouth was traveling fast. By the early 1980s, revenues had already reached 1 million dollars.

As mentioned in my previous article on Quicksilver, surfing was becoming a popular sport and the surf wear category was prime for disruption. Billabong capitalized on that trend by going big on marketing and sponsored surfing events. The goal was to get the brand known in the international scene. Licensing thus started in the early 1980s, starting with New Zealand, Japan and the US. Bob Hurley, who co-founded Billy International, became the US licensee, operating out of Orange County, California. The US market was hot for surf wear, which propelled the growth of Billabong. By early 1990s, Billabong had licensed its brand internationally, to countries such as Indonesia and South Africa. But they decided to take control over their European licensee and manage growth in that region by themselves, just like Quiksilver.

A natural step was the expansion of product lines and exploring adjacent product categories. Bad Billys was set up to cater for skateboarders while Thin Air was started to produce snowboard carriers and jackets for surfers. Everything was going in Billabong’s favor until 1998. This is when Billy International chose not to renew its license over a disagreement on the strategic direction of the company. Gordon Merchant wanted to cater for the women’s segment as well but it seemed that Bob Hurley did not like that idea. Billabong rushed to find a replacement at first but in the end, they decided to carry out the US operations by themselves.

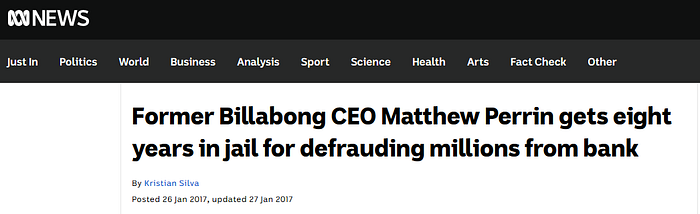

The cash infusion came from a group of investors led by Gary Pemberton and Matthew Perrin. At that point, Rena Merchant had sold her stake in the company as she was no longer with Gordon and their business relationship felt awkward. Pemberton helped the brand in its international expansion, bringing in his experience from Qantas Airways and a slew of other Australian companies. As for Perrin, the first thing I saw when I googled his name was that he was sentenced to 8 years in jail for defrauding a bank. He is also known as a corporate raider.

Now that the US operations were taken over, Billabong had to find a production facility in the US and hire and train employees to get production back on track. The US was obviously an important market, expected to contribute around 50% of total revenues. And this time, it would be pure sales rather than licensing fees. The girl’s and women’s product lines were successfully launched in late 1990s and marketing for their products were rolled out. The brand started consolidating its licensing business by purchasing licensees in Canada and New Zealand. The idea was to standardize the sourcing, marketing, employee training and store experience to ensure consistent quality and derive economies of scale.

Billabong was present in thousands of stores across the world and raked in over 200 million dollars in sales. This is when they went for an IPO in 2000. And guess what they did right after. They took over their Japanese licensee, in an attempt to compete with Quiksilver there. Then started the string of acquisitions. Von Zipper, an eyewear brand, and Element, a skateboarding apparel brand, were bought. Then Nixon and Kustom were added to the portfolio.

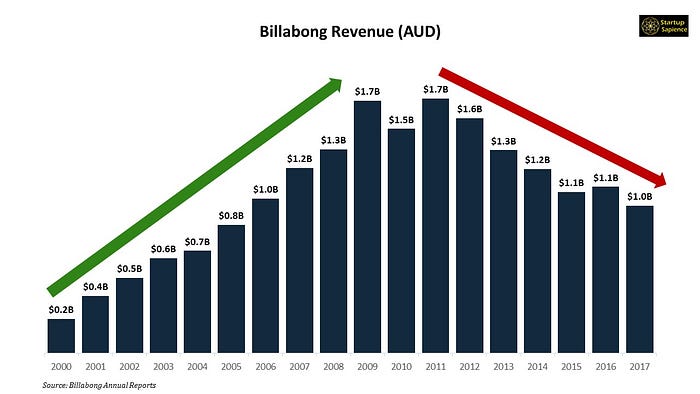

Billabong was growing at a fast clip, continuing its acquisition activity. Xcel, Tigerlily, Sector 9, DaKine, and RVCA joined the Billabong family, amongst others. As always, I plotted some financials to see how the company was progressing. Revenues grew from around 225 million dollars to over 1.7 billion dollars by 2009. But then, things took a turn for the worst. They might have been expanding too fast with the acquisitions, taking on a lot of debt. The brand had lost its appeal as it was being mass marketed through large department stores. Customers began shifting to competitors like Abercrombie & Fitch and the likes.

By 2012, the brand was struggling. It decided to undergo a major overhaul, closing down stores and laying off employees. It sold a stake in Nixon and used the proceeds to pay down some debt. TPG Capital offered to takeover Billabong but Gordon rejected it. Bain Capital and VF Corp also joined the takeover battle. But in the end, guess who lent out money to work through the restructuring. Our good old friend, Oaktree Capital, this time partnering with Centerbridge Partners. They actually had to fight for the deal as other hedge funds were vying Billabong as well.

If we look at the net income, we can see that the write offs plunged Billabong in red territory. Some of the brands, like West 49, Surfstich and Swell, were eventually sold off to generate cash inflow. Billabong ended up being bought by Quiksilver’s parent company, Boardriders, in 2018.

Do you own any Billabong branded clothes? Where do you think they went wrong? What do you think they should do to reignite sales? As always, let me know what you think.